China Tightens Digital Finance Distribution

On 24 April 2026, the People’s Bank of China (PBoC), together with the Ministry of Industry and Information Technology (MIIT), State Administration for Market Regulation (SAMR), State Financial Regulatory Administration (SFRA), China Securities Regulatory Commission (CSRC), National Intellectual Property Administration (CNIPA), Cyberspace Administration of China (CAC), and State Administration of Foreign Exchange (SAFE), jointly issued the “Administrative Measures for Online Marketing of Financial Products”.

The Measures establish a unified regulatory framework for the online distribution and marketing of financial products across licensed institutions and third-party digital platforms. The regulatory intent is to align fast-expanding platform-based financial marketing with existing financial supervision standards, reduce consumer protection risks, and close governance gaps created by algorithm-driven and influencer-led financial promotion models.

The Measures take effect on 30 September 2026, with a transition period for remediation and compliance adjustment. The measures signal a shift toward stricter oversight of digital financial marketing, requiring (international) businesses to strengthen compliance systems and reassess platform-based distribution strategies.

Executive Summary

- China introduces a unified cross-agency framework governing online financial product marketing across institutions and digital platforms.

- Regulatory scope expands to include third-party internet platforms acting as financial marketing intermediaries.

- Stronger controls are imposed on misleading advertising, algorithmic recommendations, and live-stream financial promotion.

- Clear licensing boundaries are reinforced, prohibiting unlicensed financial marketing and disguised intermediation.

- Financial institutions retain primary accountability for marketing compliance and content governance.

- Platform operators are restricted from interfering with core financial processes such as credit assessment and transaction execution.

- Full implementation is scheduled for 30 September 2026, requiring phased remediation across industry participants.

From Platform Growth to Governance Standardization

The Measures reflect a structural policy response to the rapid digitalization of China’s financial distribution channels. According to the issuing authorities, online platforms have significantly improved access to financial services and reduced distribution costs. However, the same ecosystem has also enabled fragmented oversight, inconsistent advertising practices, and elevated risks of consumer misrepresentation.

The policy aligns with broader national directives, including guidance from the 20th National Congress of the Communist Party of China and the 2023 Central Financial Work Conference, both of which emphasize unified supervision of financial activities across offline and online channels.

The regulatory shift is therefore not incremental. It represents an effort to formalize platform-based financial marketing as a fully supervised extension of the regulated financial system rather than a loosely governed digital sales channel.

Scope Expansion

A defining feature of the Measures is the explicit inclusion of third-party internet platforms within the regulatory perimeter.

The framework applies to licensed financial institutions conducting online marketing of financial products, third-party platforms (apps, websites, digital ecosystems) acting as commissioned marketing intermediaries, and local financial organizations under regional supervisory structures.

Third-party platforms are no longer treated as neutral infrastructure providers. Instead, they are formally classified as regulated intermediaries when they facilitate financial product marketing on behalf of licensed institutions.

This reclassification materially increases compliance obligations for platform operators, particularly in relation to content control, partner onboarding, and transaction routing integrity.

Licensing Discipline and Structural Restrictions

The Measures reinforce a strict “no-license, no-market access” principle for financial product promotion.

Key regulatory constraints include:

- Financial marketing must remain within approved licensing scope.

- Unlicensed entities are prohibited from promoting or facilitating financial products.

- Disguised intermediation, including indirect referral chains, is explicitly restricted.

- Platforms may not re-route users to unauthorized financial service providers.

The regulatory intent is to eliminate multi-layered distribution chains that obscure accountability and weaken supervision.

In practice, this reduces flexibility in affiliate marketing structures and significantly limits informal or semi-formal financial promotion networks that have emerged in digital ecosystems.

Standardization of Financial Communication

The Measures introduce stricter controls over financial marketing content across both institutional and platform channels.

Financial institutions are designated as the primary accountability holder for:

- Accuracy of all promotional materials.

- Internal review and compliance validation mechanisms.

- Consistency between marketing content and product risk profiles.

Digital marketing content must follow standardized communication principles:

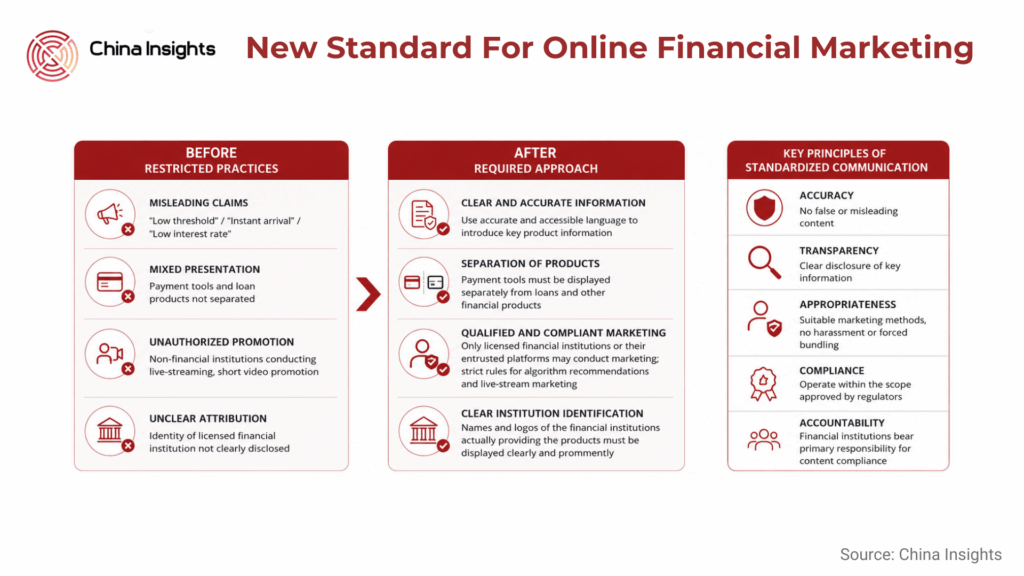

- Clear and non-misleading language requirements.

- Prohibition of exaggerated or simplified credit claims.

- Mandatory separation of payment tools and credit products in user interfaces.

- Clear identification of licensed financial institutions behind marketed products.

High-risk promotional practices are directly addressed, particularly in digital-native formats such as:

- Algorithm-driven recommendation feeds.

- Short-form video advertising.

- Live-stream financial promotion channels.

Notably, certain loan marketing expressions implying immediacy or low barriers to access are restricted, reflecting regulatory concern over behavioral nudging in consumer credit markets.

Limits on Intermediation and Influence

Third-party platforms are subject to explicit operational constraints designed to prevent functional substitution of licensed financial institutions.

Platforms are prohibited from interfering with sales execution or contract formation, conducting creditworthiness or suitability assessments, providing implicit or explicit financial advisory services, obscuring the identity of the licensed financial institution and rebranding or diluting product origin attribution.

The Measures effectively draw a hard boundary between distribution infrastructure and financial decision-making authority. This represents a significant governance clarification for platform operators whose business models integrate recommendation engines, embedded finance, and user behavioral data.

Compliance Architecture and Enforcement Timeline

The Measures will become effective on 30 September 2026, establishing a defined transition window for remediation.

Enforcement will be coordinated across multiple regulatory bodies, including: PBoC (monetary and systemic financial oversight), CSRC (capital markets regulation), SFRA (financial services supervision), CAC (digital content and platform governance), SAMR (advertising and market conduct regulation) and SAFE (cross-border financial flows).

This multi-agency structure signals that enforcement will not be siloed within financial regulation alone but will extend across advertising, cybersecurity, and platform governance domains.

What this means for business

The Measures materially reshape the operating environment for any business involved in financial product distribution, digital marketing, or platform-enabled financial services in China.

- Platform-based distribution models require structural redesign

Businesses relying on third-party ecosystems for financial product reach will need to reassess platform dependencies. Intermediation chains must be simplified, and attribution of licensed responsibility made explicit. - Marketing compliance shifts from campaign-level to system-level governance. Compliance can no longer be managed at the content review stage alone. Firms will need integrated governance systems covering content generation, algorithmic distribution logic, and partner onboarding.

- Algorithmic and AI-driven promotion will face heightened scrutiny. Recommendation systems used for financial products will require explainability, traceability, and stricter rule-based constraints to avoid unintended promotional bias or misclassification.

- Platform operators become regulated co-responsible entities. Digital platforms are no longer passive channels. They are operationally accountable for ensuring marketing integrity, requiring investment in compliance infrastructure and auditability.

- Competitive advantage shifts toward regulated capability maturity. Institutions with strong internal controls, licensing discipline, and transparent marketing systems will gain relative advantage, while loosely structured digital distribution models will face contraction.

Overall, the Measures signal a transition from growth-driven financial digitalization to a governance-first operating model, where compliance architecture becomes a core determinant of market access and scalability.

Source

https://www.gov.cn/zhengce/202604/content_7066934.htm

Author

Dr. Richard van Ostende

Related Articles