China Releases Five-Year Circular Economy Development Plan: Policy Framework for Resource Efficiency and Industrial Upgrading

On 30 June 2026, the National Development and Reform Commission formally issued the Circular Economy Development “15th Five-Year Plan” (《循环经济发展“十五五”规划》).

The plan sets medium- and long-term targets for China’s circular economy development through 2030 and 2035. It focuses on resource efficiency, waste reutilization, industrial upgrading, and the expansion of recycling systems across key sectors.

The policy reflects China’s strategic shift toward resource security, supply chain resilience, and green industrial transformation.

Executive Summary

- China has released the Circular Economy Development “15th Five-Year Plan” (NDRC, 30 June 2026), which sets binding development targets for 2030 and a structural vision for 2035.

- Key targets include a 16% increase in resource productivity by 2030 compared to 2025.

- Annual utilization of bulk solid waste is expected to reach around 4.5 billion tons by 2030.

- Annual recycling of major secondary resources is projected to reach 510 million tons by 2030.

- The circular economy industry is expected to reach RMB 8 trillion in output value by 2030.

- Policy focus includes resource reduction, improved recycling networks, and industrial upgrading.

- The plan introduces targeted strategies for bulk waste, urban mining, and “new three items” (EV batteries, wind, and solar equipment waste).

Policy Context and Strategic Drivers

The National Development and Reform Commission emphasizes that circular economy development is a core national strategy linked to resource security and green transition objectives.

China has achieved significant progress since the 18th Party Congress. By 2025, resource productivity improved by approximately 77% compared to 2012. Energy and water intensity per unit of GDP declined significantly. Bulk solid waste utilization exceeded 60%, while total recycled resource volumes surpassed 4.1 billion tons annually.

The policy also highlights external and structural pressures. Global resource competition is intensifying, and supply chain security has become a strategic priority. At the same time, China faces internal constraints, including uneven resource productivity across sectors, fragmented recycling systems, technological bottlenecks, and suboptimal industrial layout.

The 15th Five-Year Plan period is positioned as a critical phase for achieving peak carbon emissions targets and advancing structural green transformation.

Policy Framework and Development Objectives

The plan defines a multi-layered framework combining macro targets and sector-specific implementation pathways.

By 2030, China aims to increase overall resource productivity by approximately 16% compared to 2025 levels. The utilization of bulk solid waste is expected to reach around 45 billion tons cumulatively over the period. The annual recycling volume of major secondary resources is projected to reach 5.1 billion tons. The circular economy industry is expected to reach a total output value of RMB 8 trillion, reflecting sustained high-growth expansion.

By 2035, China aims to establish a mature circular economy system. Resource utilization efficiency is expected to reach advanced international levels. This indicates a transition from expansion-driven growth to efficiency-driven industrial maturity.

The policy integrates circular economy development with broader national priorities, including industrial upgrading, emissions reduction, and resource independence.

Resource Reduction and Efficiency Gains

The first policy pillar focuses on reducing resource consumption at the source. The plan promotes green product design, cleaner production processes, and sustainable consumption patterns. These measures are intended to improve upstream efficiency in industrial and consumer systems.

The government also emphasizes the need to improve resource productivity across industrial value chains. This includes optimizing material use in manufacturing, construction, and agriculture. The NDRC highlights that improving upstream efficiency is essential to reduce dependence on primary resource extraction and stabilize long-term supply conditions.

Expansion of Recycling and Resource Recovery

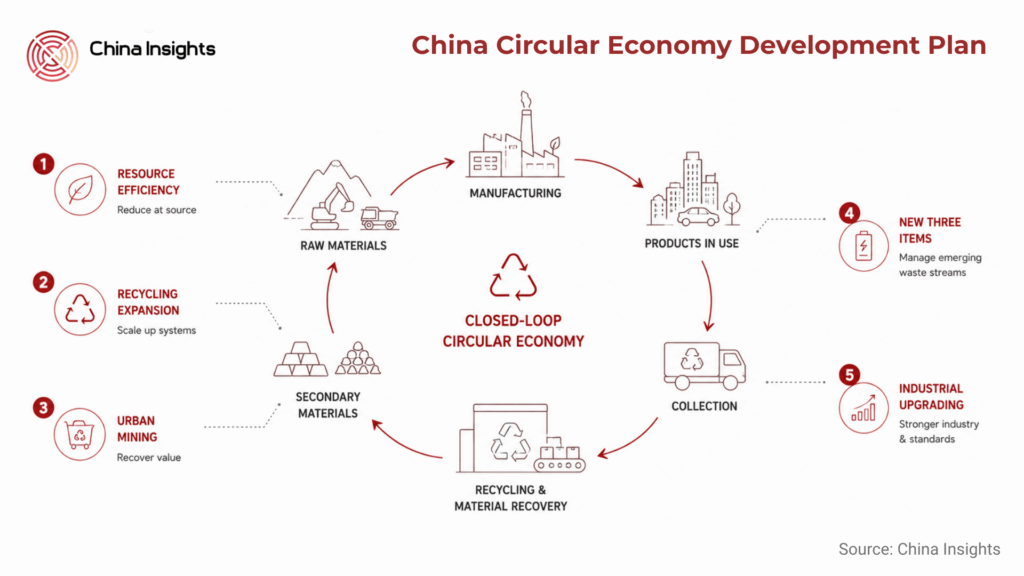

The second pillar focuses on strengthening domestic secondary resource supply. China plans to expand recycling systems across industrial, agricultural, and construction sectors. The goal is to significantly increase the volume of recoverable materials entering formal recycling channels. The policy identifies large-scale solid waste categories such as coal gangue, fly ash, tailings, and construction waste as priority streams for expanded utilization. These materials will be increasingly treated as resource inputs rather than environmental liabilities. In parallel, the plan emphasizes expansion of recycling systems for secondary metals and materials, including steel, non-ferrous metals, plastics, and textiles. The policy also signals a gradual expansion of overseas secondary resource utilization channels. This includes improved import management mechanisms, streamlined regulatory procedures, and broader access to international recycled material markets.

Sector-Specific Circular Economy Development

The third pillar introduces targeted interventions for specific waste streams and industrial categories. The plan identifies three strategic focus areas:

- Bulk solid waste utilization. This includes expanding the utilization of industrial by-products such as coal-based residues and mining waste, with the aim of increasing absorption capacity across downstream industries.

- Urban mining development. This refers to high-value recovery from end-of-life products, including vehicles, electrical appliances, steel scrap, non-ferrous metals, plastics, and textiles. The policy emphasizes improved dismantling standards and formal recycling channels.

- Emerging “new three items” waste streams. These include used power batteries, decommissioned wind power equipment, and retired photovoltaic systems. The plan highlights the need to strengthen regulatory frameworks, clarify disposal responsibilities, and establish standardized collection systems.

These measures reflect increasing attention to emerging environmental risks associated with rapid renewable energy deployment.

Industrial Upgrading and Regulatory Modernization

A key feature of the plan is its focus on upgrading the circular economy industry itself. The NDRC identifies structural weaknesses in the sector, including fragmented enterprises, weak economies of scale, uneven technological capacity, and insufficient digitalization in monitoring systems.To address these issues, the policy proposes strengthening legal and regulatory frameworks, improving technical standards, and enhancing statistical and evaluation systems.

The plan also encourages the development of leading enterprises to consolidate market structure and improve industrial efficiency. This reflects a shift toward more consolidated and technology-intensive recycling industries. Policy support mechanisms will include financial incentives, regulatory alignment, and improved oversight systems to reduce low-quality competition.

Governance Structure and Implementation Mechanism

The implementation framework relies on coordinated governance between central and local authorities. The NDRC will act as the lead coordinating body for circular economy development. It will be responsible for policy integration, task decomposition, monitoring, and performance evaluation. Local governments are required to implement region-specific action plans, aligned with national targets. Sectoral ministries will be responsible for policy execution within their respective domains. The plan also emphasizes public participation, international cooperation, and awareness-building to support systemic adoption of circular economy principles.

What this means for business

The policy signals a structural expansion of China’s circular economy sector, with increasing demand for recycling technologies, waste processing infrastructure, and secondary material supply chains. Industrial firms operating in metals, construction materials, automotive recycling, and electronics recovery will face stricter regulatory frameworks but also expanded market opportunities.

Manufacturers will need to adjust production processes to align with stricter resource efficiency requirements and incorporate higher shares of recycled materials. This will particularly affect sectors such as automotive, electronics, and construction.

For recycling and waste management companies, the policy supports consolidation and scale expansion. Smaller operators may face competitive pressure as the market shifts toward standardized and regulated industrial systems.

Technology providers in sorting, material recovery, digital tracking, and lifecycle management systems are likely to benefit from increased policy-driven investment.

Overall, the plan reinforces circular economy development as a core component of China’s industrial and resource strategy through 2035.

Source

https://www.gov.cn/zhengce/202607/content_7074227.htm

Author

Dr. Richard van Ostende

Related Articles