Exploring “Vehicle - Battery Separation” Insurance Models in China: Regulatory Direction and Market Implications Introduction

Chinese authorities are increasingly exploring new insurance and risk-sharing mechanisms to support the commercialization of electric vehicles (EVs), particularly under battery swapping and “vehicle–battery separation” models. Regulatory discussions are focusing on insurance innovation aligned with new mobility business models. The initiative reflects the structural evolution of China’s EV ecosystem, where asset ownership, operational risk, and insurance liability are being redefined due to battery leasing and swapping systems.

Executive Summary

- China is exploring insurance mechanisms tailored to vehicle–battery separation models in the EV sector.

- The policy direction aims to address asset ownership fragmentation and risk allocation challenges.

- Insurance innovation is linked to the growth of battery swapping and leasing business models.

- Regulators are focusing on improving risk pricing, liability attribution, and claims efficiency.

- The framework supports broader EV ecosystem standardization and financial infrastructure development.

- The initiative has implications for automakers, battery operators, insurers, and mobility platforms.

Policy Context and Regulatory Direction

The policy discussion on “vehicle–battery separation” insurance models is presented in a policy interpretation article titled “Exploring ‘vehicle–battery separation’ insurance models” (“探索‘车电分离’等保险模式”) published by Chinese authorities. The article reflects ongoing regulatory interest in aligning insurance systems with new energy vehicle (NEV) business models. The publication does not constitute a formal regulation but provides interpretive guidance on policy direction and market experimentation.

The policy focus is linked to the structural shift in NEV ownership models, where batteries are increasingly treated as separable, depreciable, and leasable assets rather than fixed vehicle components.

Structural Characteristics of Vehicle–Battery Separation

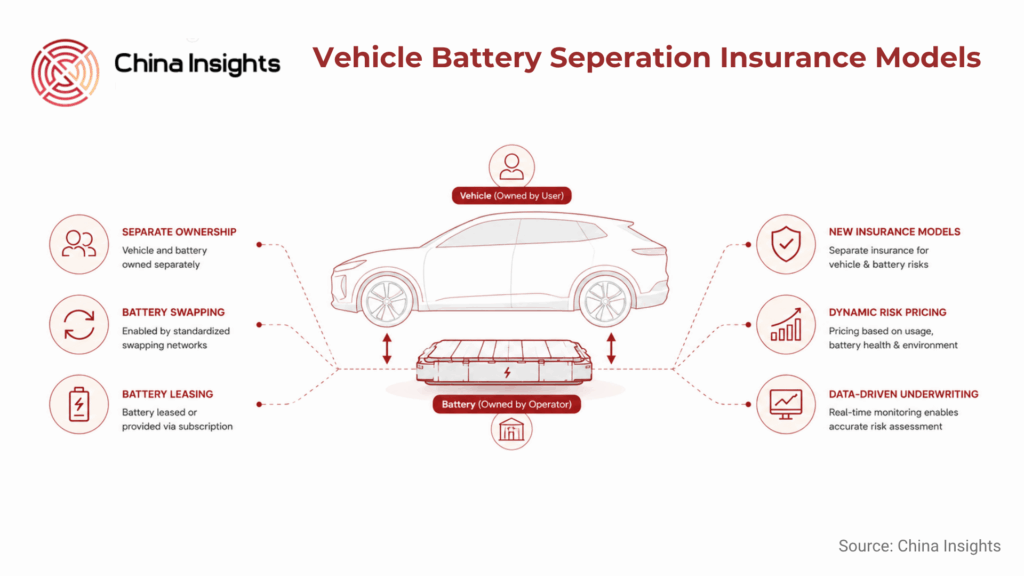

The “vehicle–battery separation” model refers to a system where the vehicle body and the battery are owned or financed separately. In many implementations, the vehicle is sold without the battery, while the battery is leased or provided via subscription or swapping networks. This model is closely associated with battery swapping ecosystems. Under this structure, users pay for battery usage rather than ownership. Battery operators retain ownership and manage charging cycles, maintenance, and lifecycle optimization. The separation of ownership introduces new complexity in asset classification, depreciation, and risk responsibility allocation. These structural characteristics directly affect insurance design.

Insurance Model Innovation and Risk Allocation

The core policy challenge identified in the interpretation article is the mismatch between traditional auto insurance frameworks and separated asset ownership structures. In conventional vehicle insurance, risk is primarily linked to a single owner-operator structure. Under vehicle–battery separation, risk is distributed across multiple stakeholders:

- Vehicle owner

- Battery owner or operator

- Battery swapping service provider

- Charging infrastructure operator

This fragmentation requires redefinition of insured objects and liability boundaries. Insurance innovation is therefore focused on developing differentiated coverage structures. These include separate insurance products for vehicle body risk and battery-related operational risks. The policy direction also encourages clearer attribution of accident responsibility and asset damage liability.

Battery Lifecycle Risk and Insurance Pricing Mechanisms

A key issue in the policy discussion is the lifecycle management of EV batteries. Batteries are high-value assets with performance degradation over time, influenced by usage cycles, charging behavior, and environmental conditions.

Under separation models, battery operators retain responsibility for performance and residual value. This introduces demand for more granular insurance pricing mechanisms based on:

- Usage intensity

- Charging cycles

- Battery health data

- Operational environment

The policy direction suggests increasing reliance on data-driven risk assessment models. This includes integration of real-time monitoring systems and digital tracking of battery condition. Insurance pricing is expected to shift from static vehicle-based premiums to dynamic asset-based risk models.

Role of Battery Swapping Ecosystems

Battery swapping infrastructure plays a central role in enabling vehicle–battery separation models. Operators manage centralized charging, standardized battery pools, and automated swapping stations. From an insurance perspective, this introduces centralized risk pooling mechanisms. Battery assets are managed at scale, allowing for more standardized risk assessment and potentially lower volatility in claims. However, concentration of battery assets also introduces systemic risk exposure. Large-scale failure, operational disruption, or safety incidents within swapping networks could generate correlated insurance claims. Regulators are therefore expected to monitor systemic risk accumulation within battery swapping ecosystems.

Data Infrastructure and Digital Risk Management

The policy interpretation emphasizes the importance of digital infrastructure in enabling new insurance models. Battery health monitoring, vehicle telemetry, and platform-based usage data are critical inputs for underwriting. The integration of data systems supports:

- Real-time risk monitoring

- Predictive maintenance models

- Fraud prevention in claims processing

- Dynamic insurance pricing

This reflects a broader regulatory trend in China toward data-enabled insurance supervision and digital risk governance. Insurance companies are expected to increasingly rely on collaboration with EV manufacturers and battery operators to access standardized datasets.

Market Participants and Industry Impact

The development of vehicle–battery separation insurance models affects multiple industry stakeholders. Automakers may need to redesign product architectures to accommodate modular battery systems. Battery manufacturers and operators are likely to expand into asset management and lifecycle service businesses. Insurance companies face structural adjustments in underwriting models and product design. Traditional motor insurance products may need segmentation into vehicle body insurance, battery insurance, and operational liability coverage. Mobility platform operators and battery swapping networks will become central nodes in the risk distribution system.

Regulatory Coordination and Standardization Needs

A key regulatory challenge is standardization across fragmented industry participants. The policy interpretation highlights the need for consistent definitions of insured assets, liability boundaries, and technical standards. Without standardization, insurance products may face inefficiencies in claims resolution and cross-platform interoperability. Regulatory coordination is expected to involve insurance regulators, transportation authorities, and energy system regulators to ensure alignment across sectors.

Risk Considerations and Structural Constraints

While the model offers efficiency gains, several structural risks remain. First, asset ownership fragmentation increases legal complexity in accident liability determination. Second, data asymmetry between operators and insurers may affect pricing accuracy. Third, operational concentration in swapping networks may create systemic exposure risks. These constraints suggest that insurance innovation will likely proceed in a phased manner, with pilot programs preceding large-scale rollout.

What this means for business

The exploration of vehicle–battery separation insurance models signals a structural shift in China’s NEV ecosystem from integrated ownership toward modular asset systems.

- For automakers and battery operators, this creates opportunities to develop integrated service ecosystems combining hardware, leasing, and insurance-linked revenue streams.

- For insurers, the transition requires redesigning underwriting frameworks around data-driven and asset-specific risk models. Collaboration with platform operators will become essential.

- For investors and mobility service providers, the policy direction indicates long-term support for battery swapping infrastructure and digital insurance integration, but with increasing regulatory emphasis on standardization and systemic risk control.

Overall, the initiative reflects a broader transformation of China’s EV industry toward platform-based asset management and digitally enabled financial services.

Source

https://www.gov.cn/zhengce/202606/content_7073145.htm

Author

Dr. Richard van Ostende

Related Articles