China's State Council Signals Stronger Focus on Audit Rectification and Government Accountability

China’s leadership has once again highlighted the strategic role of auditing in strengthening governance and improving the effectiveness of public administration. During a recent State Council Executive Meeting, policymakers reviewed the annual audit report on the execution of the central government budget and other fiscal revenues and expenditures.

The meeting emphasized that audit findings must not be treated as a procedural exercise. Instead, identified issues should be addressed through comprehensive rectification measures designed to improve policy implementation, fiscal discipline, and institutional governance.

The discussion reflects the increasingly important role that auditing plays within China’s broader governance framework. In recent years, audits have become a key mechanism for identifying inefficiencies, strengthening accountability, mitigating risks, and ensuring that public resources are used effectively.

For businesses and investors, the latest policy signals provide additional insight into the government’s priorities regarding compliance, financial oversight, and administrative effectiveness.

Executive Summary

China’s State Council has reinforced the importance of addressing issues identified through government audits, emphasizing accountability, fiscal discipline, and policy effectiveness.

Key takeaways include:

- The State Council Executive Meeting reviewed the 2025 Central Budget Execution and Other Fiscal Revenue and Expenditure Audit Report.

- Authorities stressed that all audit findings must be treated seriously and rectified in a timely manner.

- The government emphasized the importance of translating audit results into improved governance and more effective policy implementation.

- Particular attention will be given to fiscal management, the use of public funds, major investment projects, and the implementation of national policies.

- Audit rectification will be linked more closely to accountability mechanisms and long-term institutional improvements.

- The policy direction signals continued efforts to strengthen transparency, efficiency, and risk management within China’s public sector.

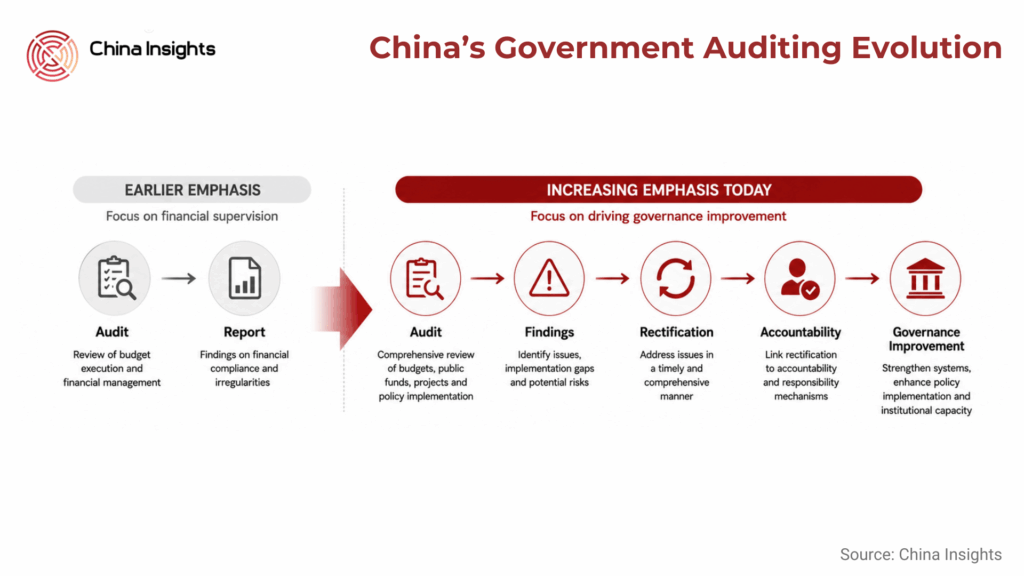

Audit Oversight as a Governance Tool

The State Council’s discussion highlights how auditing has evolved beyond traditional financial supervision to become an important instrument of public governance.

Government audits now play a critical role in evaluating whether public funds are being used efficiently, whether policy objectives are being achieved, and whether administrative agencies are fulfilling their responsibilities. The annual audit process provides policymakers with a comprehensive assessment of budget execution, project implementation, and financial management across government departments and state institutions.

By strengthening the link between audits and policy implementation, authorities aim to improve the quality of governance while ensuring that fiscal resources support national development priorities more effectively.

The latest meeting demonstrates that audit findings continue to receive high-level political attention and are viewed as an important source of information for decision-making.

Rectification Becomes the Priority

A central message emerging from the State Council meeting is that identifying problems is only the first step. Equal emphasis is being placed on ensuring that audit findings lead to concrete corrective actions.

Authorities stressed that audit issues must be addressed comprehensively and that responsible organizations should develop clear rectification plans. The objective is not merely to resolve individual cases but to address underlying causes that may contribute to recurring problems.

This approach reflects a broader trend in Chinese governance toward strengthening implementation and accountability. Policymakers increasingly emphasize policy outcomes rather than policy announcements alone.

As a result, government departments, local authorities, and state-owned entities are likely to face increased scrutiny regarding how quickly and effectively they respond to audit findings.

Improving Fiscal Discipline

One of the primary functions of China’s audit system is to strengthen fiscal management and safeguard public finances.

The State Council meeting highlighted the need to improve budget execution, strengthen financial controls, and enhance the efficiency of public spending. This aligns with broader efforts to improve fiscal sustainability amid growing demands for public investment, social services, and economic support measures.

Audit findings often reveal weaknesses in project management, fund allocation, procurement practices, and expenditure controls. Addressing these weaknesses is considered essential for ensuring that fiscal resources generate the intended economic and social outcomes.

The emphasis on fiscal discipline also reflects China’s commitment to maintaining financial stability while supporting long-term development objectives.

Strengthening Policy Implementation

Beyond financial management, audits increasingly assess whether major national policies are being implemented effectively.

The State Council emphasized that audit work should support the implementation of key national strategies and help identify obstacles that may hinder policy execution. This includes monitoring major infrastructure projects, industrial policies, environmental initiatives, and social development programs.

By using audit findings to identify implementation gaps, policymakers aim to improve coordination among government departments and enhance the effectiveness of public administration.

This focus is particularly important as China advances a growing number of complex policy initiatives related to industrial upgrading, technological innovation, green development, and domestic demand expansion.

Enhancing Risk Prevention and Control

The State Council’s remarks also highlight the role of audits in identifying and mitigating risks.

Government audits are increasingly used to detect potential financial, operational, and governance risks before they develop into larger systemic problems. Areas of concern may include debt management, project execution risks, inefficient use of public resources, and weaknesses in internal control systems.

Strengthening audit-based risk management aligns with China’s broader emphasis on preventing major economic and financial risks. Early identification of vulnerabilities allows policymakers to implement corrective measures before significant negative consequences emerge.

The integration of audit supervision with risk management therefore serves both governance and economic stability objectives.

Accountability and Institutional Reform

A notable aspect of the State Council’s position is the emphasis on accountability.

Authorities indicated that audit findings should contribute not only to correcting specific problems but also to improving institutional systems and governance mechanisms. In practice, this means that recurring issues may trigger reviews of administrative processes, regulatory frameworks, or management practices.

The objective is to transform audit supervision into a mechanism that promotes continuous improvement rather than one-time correction.

This approach supports China’s broader governance agenda, which places increasing emphasis on performance management, administrative efficiency, and evidence-based policymaking.

For government agencies and public institutions, stronger accountability requirements are likely to increase the importance of compliance, internal controls, and performance monitoring.

Implications for State-Owned Enterprises

Although the State Council meeting primarily focused on government audits, the policy direction also carries implications for state-owned enterprises (SOEs).

SOEs frequently participate in major national projects, manage significant public resources, and play key roles in strategic sectors. As a result, audit findings related to state-owned entities often attract particular attention.

The continued emphasis on accountability and rectification suggests that SOEs may face increasing expectations regarding governance standards, financial management, project execution, and compliance practices.

For organizations working with SOEs, stronger oversight may contribute to improved transparency and more rigorous management processes over time.

Governance Modernization Remains a Priority

The State Council’s discussion should be viewed within the broader context of China’s efforts to modernize governance systems and improve the quality of public administration.

Over the past decade, authorities have increasingly focused on enhancing regulatory effectiveness, strengthening supervision, improving fiscal management, and promoting accountability across government institutions.

The latest emphasis on audit rectification reflects a continued commitment to ensuring that governance systems evolve alongside China’s economic and social development objectives.

Rather than introducing a new regulatory framework, the meeting reinforces the importance of implementation, execution, and institutional learning as key components of effective governance.

What This Means for Business

The State Council’s focus on audit rectification signals that compliance, accountability, and effective implementation will remain central themes within China’s governance environment.

For businesses operating in China, particularly those involved in government procurement, infrastructure projects, public-private partnerships, or cooperation with state-owned enterprises, stronger audit oversight may translate into increased attention to documentation, compliance, and performance management.

Companies should expect continued scrutiny regarding the use of public funds, project execution quality, and adherence to regulatory requirements. Organizations with strong internal controls, transparent reporting systems, and robust compliance frameworks are likely to be better positioned in this environment.

The policy direction also suggests that authorities will continue prioritizing efficiency and effectiveness in the implementation of major policy initiatives. Businesses aligned with national development priorities may benefit from a more disciplined and accountable policy environment.

More broadly, the State Council’s message reinforces the importance of governance quality as a key factor supporting China’s economic development and policy execution capabilities.

Source

Author

Dr. Richard van Ostende

Related Articles